Introduction

Ask any middle-class Indian today how they feel about money, and you’ll hear a familiar mix of frustration and confusion. Salaries have grown, yes—but so have rents, school fees, medical costs, and lifestyle expectations. On paper, incomes look better than they did a decade ago. In reality, savings feel thinner, and long-term security feels harder to reach.

This disconnect is what’s worrying people the most. Are we earning more but building less wealth? And more importantly, what can realistically be done about it? This article breaks down why middle-class wealth is under pressure and how Indians—quietly and practically—are adapting to protect and rebuild their financial footing.

Real-World Experience: What I’m Seeing Across Households

In my experience, the middle-class squeeze isn’t theoretical—it shows up in everyday decisions. I’ve seen families delay home purchases, professionals cut back on discretionary spending, and dual-income households still feel financially stretched.

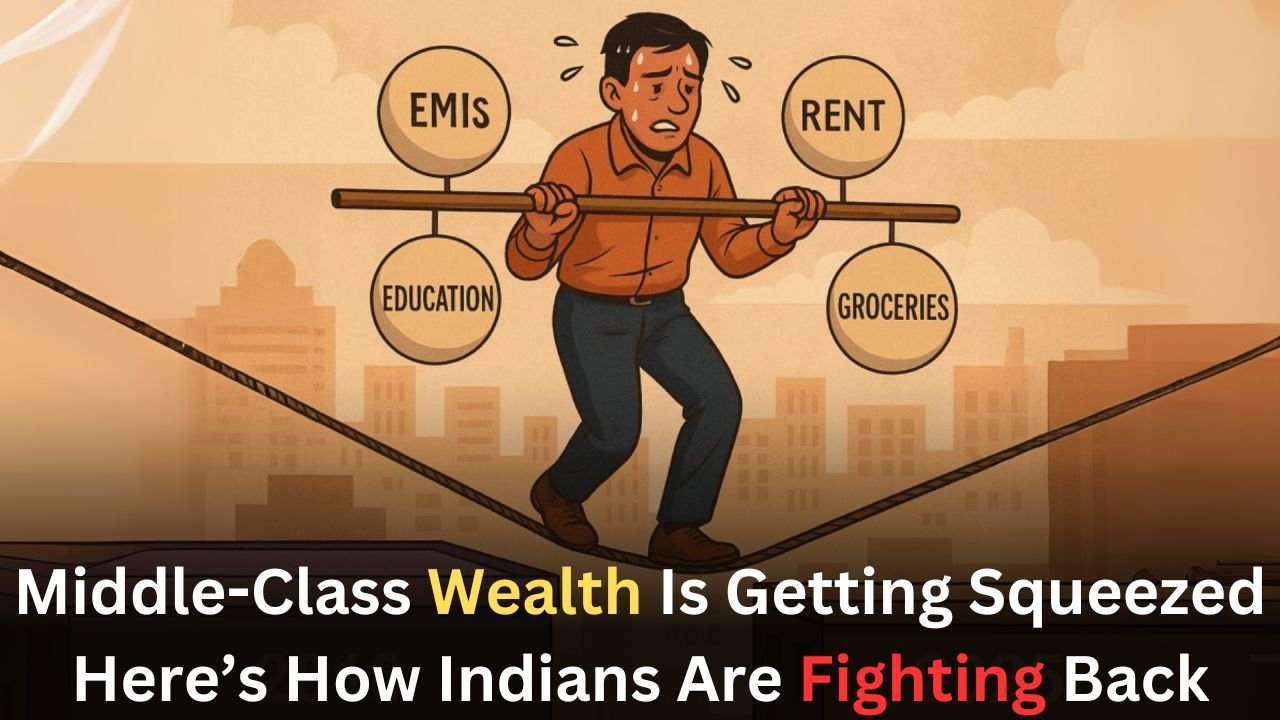

What I noticed during regular conversations and budget reviews is that the pressure doesn’t come from reckless spending. It comes from fixed costs creeping up faster than income growth. EMIs, insurance premiums, education expenses, and healthcare don’t feel optional anymore. Even disciplined savers are finding it harder to increase net worth at the same pace as before.

The positive side? People aren’t giving up. They’re adjusting—sometimes subtly, sometimes decisively.

Why Middle-Class Wealth Is Feeling the Pinch

The core issue isn’t one single factor. It’s the combination.

Inflation has quietly reshaped household budgets. Essentials consume a larger share of income, leaving less room for investing. At the same time, traditional “safe” options like fixed deposits no longer deliver meaningful real returns after tax and inflation.

There’s also lifestyle compression. The middle class today is expected to fund quality education, private healthcare, better housing, and digital convenience—all of which cost significantly more than they used to. Wealth isn’t just about income anymore; it’s about how efficiently that income compounds over time. And that efficiency has taken a hit.

How Indians Are Actually Fighting Back

The response from the middle class hasn’t been dramatic—but it’s been smart.

Instead of chasing flashy returns, many are focusing on control. They’re rethinking expenses, renegotiating fixed costs, and becoming more intentional about where money flows. In real life, this looks like choosing smaller homes, delaying upgrades, and prioritizing cash flow over status purchases.

On the investment side, there’s a visible shift away from passive complacency. People are learning, comparing, and asking better questions. They’re not abandoning safety—but they’re no longer relying on it alone.

Investment Behavior: From Safety-First to Balance-First

One noticeable change is how middle-class investors think about risk.

Earlier, safety meant parking money in FDs, insurance-linked products, or low-yield schemes. Today, safety increasingly means diversification. Equity mutual funds, SIPs, and hybrid products are being used not for quick gains, but for long-term protection against inflation.

In practical terms, this helps money grow with the economy rather than lag behind it. The benefit isn’t immediate gratification—it’s resilience. Families that adopt this mindset are better positioned to absorb shocks without derailing their future plans.

Comparison: Old Middle-Class Strategy vs New-Age Approach

The traditional middle-class strategy was straightforward: earn steadily, save aggressively, avoid risk. It worked in a slower, cheaper economy.

The newer approach is more adaptive. Income is still important, but flexibility matters more. Instead of locking money away indefinitely, people prefer liquidity with growth potential. Instead of one large goal, they plan for multiple smaller milestones.

Huawei Pura 80 Ultra Review : Photography Powerhouse with 1-Inch Sensor and Kirin 9020 Muscle

The old strategy suits those nearing retirement with limited risk appetite. The new approach works better for earning households trying to build wealth despite rising costs. The mistake is clinging to old methods in a changed environment.

Skills and Side Incomes: An Underestimated Shift

Another quiet but powerful trend is skill-based income diversification.

Middle-class professionals are upgrading skills, freelancing, consulting, or building small digital income streams. Not to become millionaires—but to reduce dependence on a single salary.

In my observation, even modest additional income creates psychological relief. It provides margin. And margin is what the middle class needs most right now.

Pros and Cons of the Middle-Class Fightback

Pros

- More informed financial decision-making

- Better diversification and inflation awareness

- Reduced dependence on traditional low-yield options

- Greater focus on long-term stability

Cons

- Requires learning and active involvement

- Mistakes are possible during transition

- Emotional discomfort with market-linked products

- Progress feels slow initially

The fightback isn’t glamorous—but it’s grounded.

Frequently Asked Questions

Is the middle class really losing wealth in India?

Not losing outright, but struggling to grow it meaningfully after inflation and rising costs.

Are investments riskier for the middle class now?

Not necessarily. The risk comes from not adapting. Staying under-invested can be riskier long-term.

Can one salary still support middle-class life comfortably?

It depends on location and lifestyle. Dual incomes or additional income sources offer more stability.

What’s the biggest mistake middle-class families make today?

Assuming old financial strategies will still work unchanged in a new economic reality.

Final Verdict: Who Needs to Act—and How Urgently

If you’re middle class and feel like you’re working harder but moving slower financially, that feeling is valid. The system has changed. Costs have risen. Expectations have shifted.

Those who adapt—by learning, diversifying, and staying flexible—are managing to protect and even grow wealth despite the squeeze. Those who rely solely on outdated methods may feel increasingly trapped.

The middle class isn’t powerless. But staying still is no longer neutral—it’s costly.